This window allows the user to apply and process a loan for a group and individual client. To be able to process a loan application, the clients must have been registered under Clients.

Note that processing a group loan goes through four stages (The Loan application window presents four tabs) whereas processing an individual loan goes through three stages (The Loan application window presents three tabs).

The LPF application screen supports different loan products, installment types, interest calculation methods, grace periods, loan funds, interest payment methods etc. The feature also supports balloon loan payments, allows users to create repayment schedules with savings amounts to be paid with each installment either as a percentage or a flat amount, checks the availability of savings required to guarantee the loan, provides flexibility to calculate interest in days or months, etc

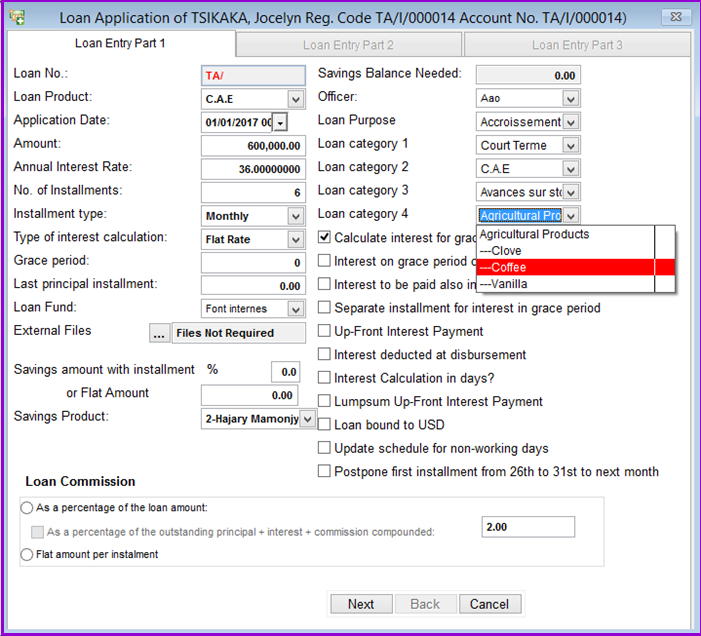

To apply for aloan, go to Loan/Loan application, the following screen appears:

Loan Nº: The system can generate this number automatically, however; if you want to be able to modify the number then you go to the menu System/ Configuration/Loans and check Loan number modifiable at application.

Loan product: From the drop down menu, you can select the loan product from which the loan application will be processed. For the loan products to appear in the drop down you need to have added them under System/ Configuration/Products and you select the product type as loans.

Application date: Enter application date here, e.g., "01/01/2015" or click on the date picker situated at the extreme right of the date box.

Amount: Specify the amount of money applied for e.g., "600,000/=".

Annual Interest Rate: Enter the annualized interest rate here, for instance if you charge 3% per month, this translates to 36 % i.e. (3*12)

No. of Installments: Enter the number of installments for the specified loan applied here.

Installment type: From the drop down menu, select the appropriate installment type. They range from Daily to Annual this can vary from product to product.

Type of Interest calculation: Loan Performer offers two types of interest calculation methods.

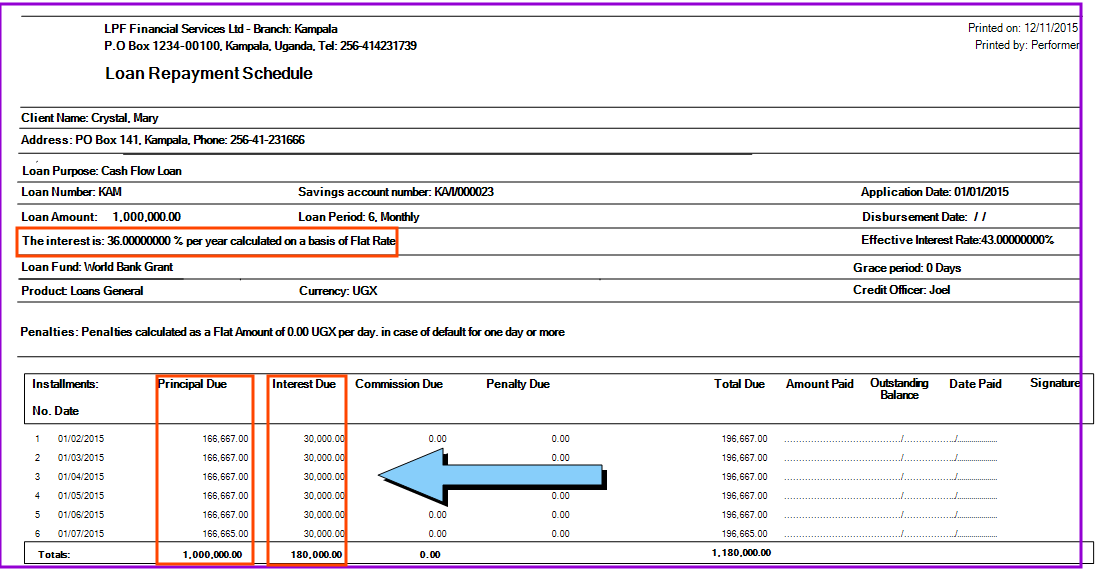

Flat rate: With this method, interest is paid on the entire loan spread throughout the duration of the loan period with equal principle and interest payments, each payment therefore includes interest.

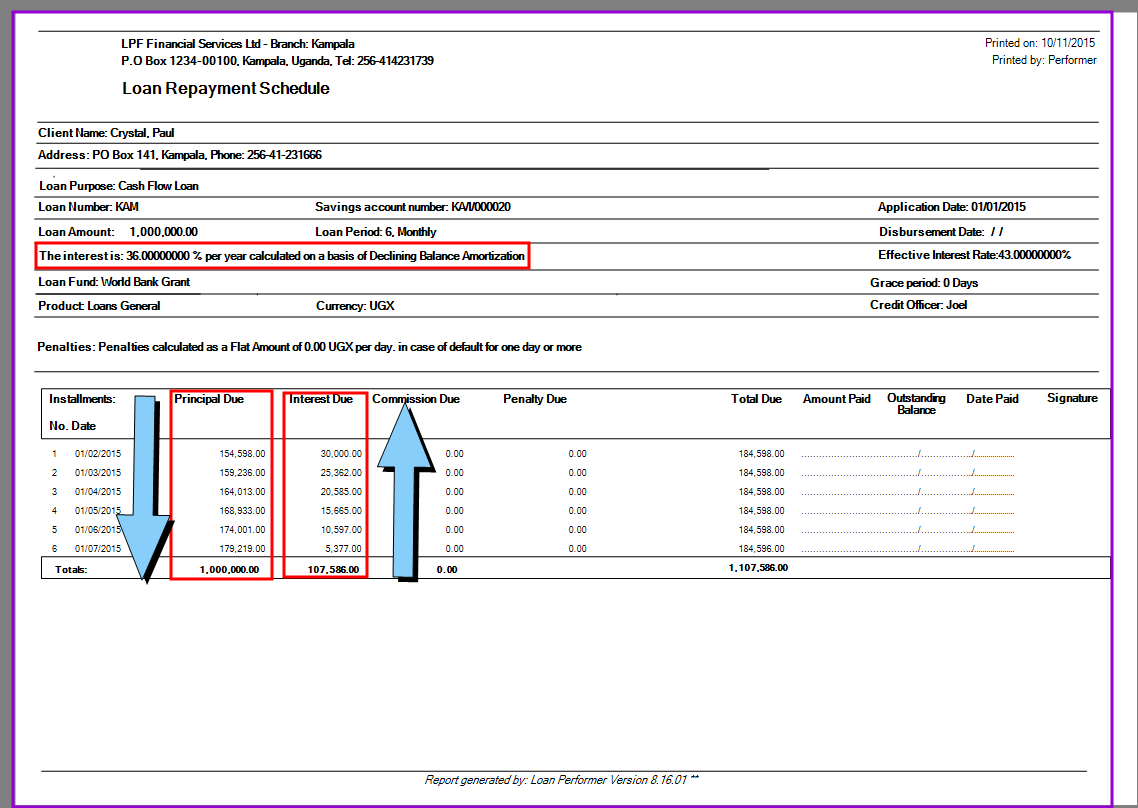

Declining balance: Since interest is charged on outstanding principle balance, the actual amount of interest charged gradually declines over time with payments made. In loan performer under declining balance are two interest calculation types:

Declining balance amortization: With amortization, total amounts per installment are equal (annuities), but principal payment per installment is increasing while interest amount is declining. This is the equivalent of the PMT function in Excel (See the following image).

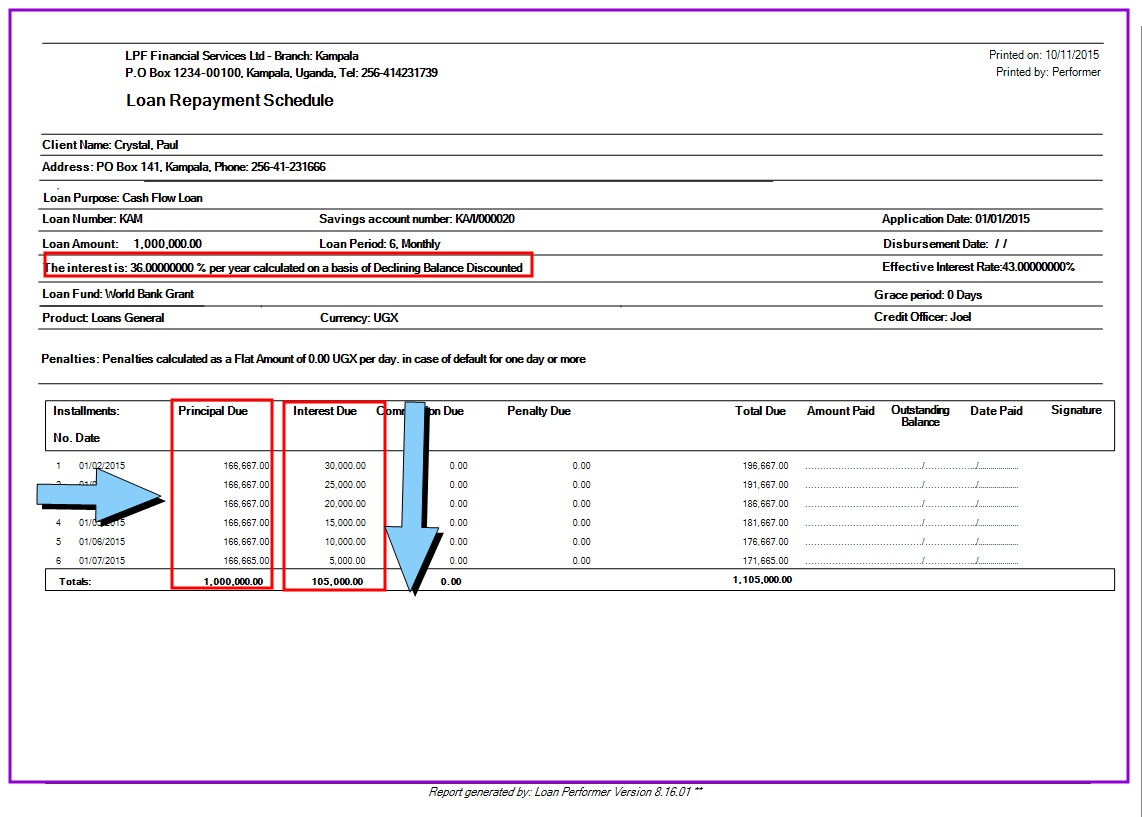

Declining balance discounted: With discounted, you get equal principal amounts and declining interest amounts per installment as shown below:

Note that you can also set the loan amount, annual interest rate, grace period, nº of installments per loan product at System\Configuration\Loan product setting\ for individual and group loans. These will then appear at loan application as defaults.

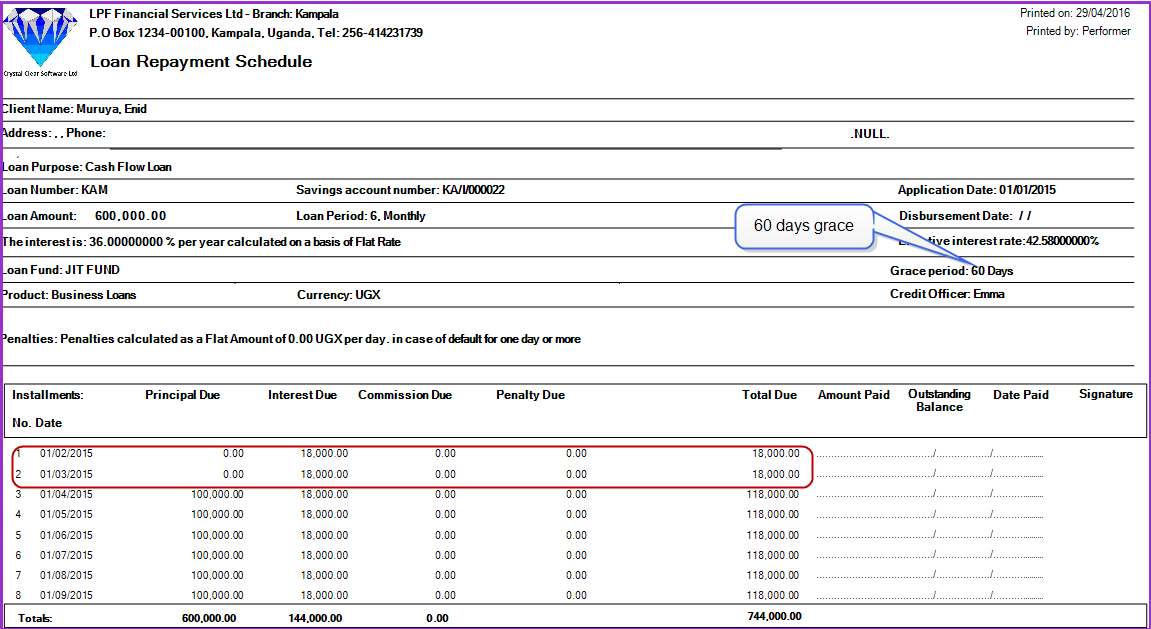

Grace period: When this option is checked, the system allow the user to specify a period of time that allows a client not make loan payments of installments that are due without being penalized. In this field enter the number of days for loans that grace periods have been provided. This should be related to the installment type of the loan.

Loan Commission: Enter the loan commission here. This is a charge that is paid with the installments. It can be entered either as a flat amount or as a percentage of the loan at System/Configurations/Loan Product Settings/Fees Settings. The commission amount will be split over the number of loan installments.

Note:

1. In this case you prefer your clients to pay loan commission gradually with each installment. Loan Performer gives the user the choice of levying loan commission either at application or disbursement. For more information, go to the menu System/Configuration/Loan Product Settings/Loan GL accounts settings part 1.

2. Note that importation of Loan commission is only possible when it is made compulsory under System/Configuration/Loan Product Settings/Fees. Other wise the importation feature will not appear under the menu Loans/Loan Importations. Other fees can also be made compulsory before application, before approval, before disbursement and at disbursement.

3. In the Loan Performer menu "System/Configuration/Loan Product Settings/Fees", you can define the amount and when the loan fees should be levied. This can be at loan application, before approval, after approval or at loan disbursement. You may also tick the corresponding check boxes to make payment of these fees compulsory.

5. When you decide to levy the loan fees after application by specifying the amounts under the menu "System/Configuration/Loan Product Settings/Fees", an additional feature "Loan fees before approval"appears in the loans module, otherwise it won't be displayed on the Loan Performer interface.

6. When you decide to levy the loan fees before disbursement by specifying the amounts under the menu "System/Configuration/Loan Product Settings/Fees", an additional feature "Loan fees after approval"appears in the loans module, otherwise it won't be displayed on the Loan Performer interface.

7. When you decide to levy the loan fees during disbursement by specifying the amounts under the menu "System/Configuration/Loan Product Settings/Fees", the disbursement screen will appear with the amount specified above, otherwise it won't be displayed on the Loan Performer interface.

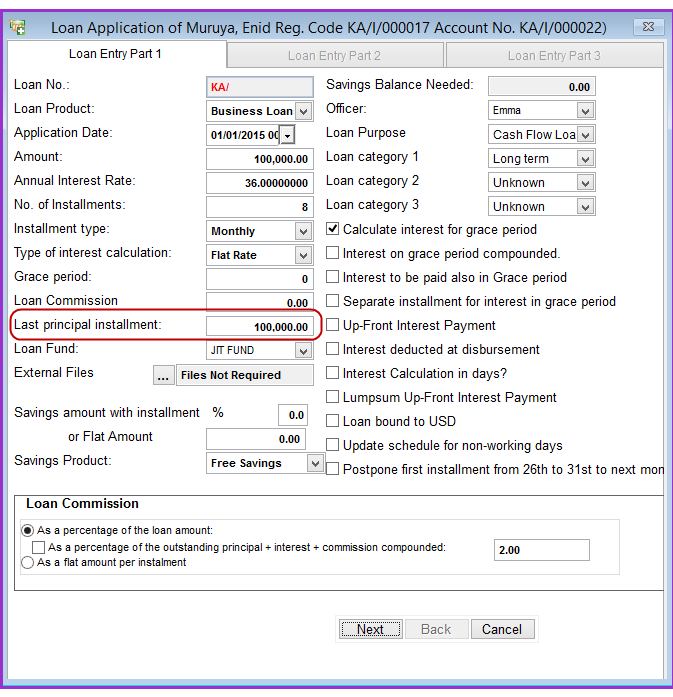

Last Principal Installment: The system gives the user the option to set the principal amount that client will pay last. This is called balloon payment and may be favorable to clients like farmers who may want to pay the principle upon harvest. As an example, consider a loan of 100,000 UGX at an annual interest rate of 36% per year for 8 months with a balloon repayment at the end and with interest on flat rate basis (See the following image):

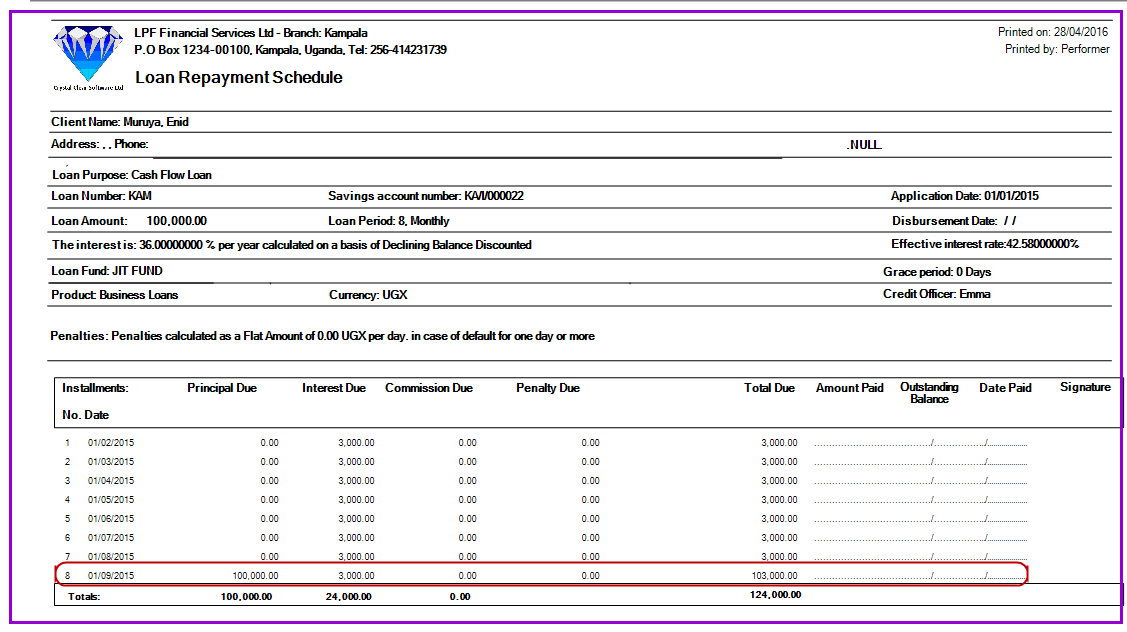

The repayment schedule appears as follows:

From the above schedule, you will notice that there are seven (7) interest-only installments plus one interest installment paid with the entire principal amount plus interest, making a total of eight (8) installments

Loan Fund: Select the fund from which this loan is going to be disbursed. This needs to be set under System/Configuration/Funds. In case of insufficient fund, the user wont be able to proceed and the system returns the following message:

Please note that the date of loan application should be after the date of creation of the loan fund otherwise the system will return the message "This fund is still empty; you need to enter transactions for this fund" even if you have already put money into the fund. This validation occurs if you have activated the option "Always check availability of funds at Loan Application" under "System/Configuration/Funds".

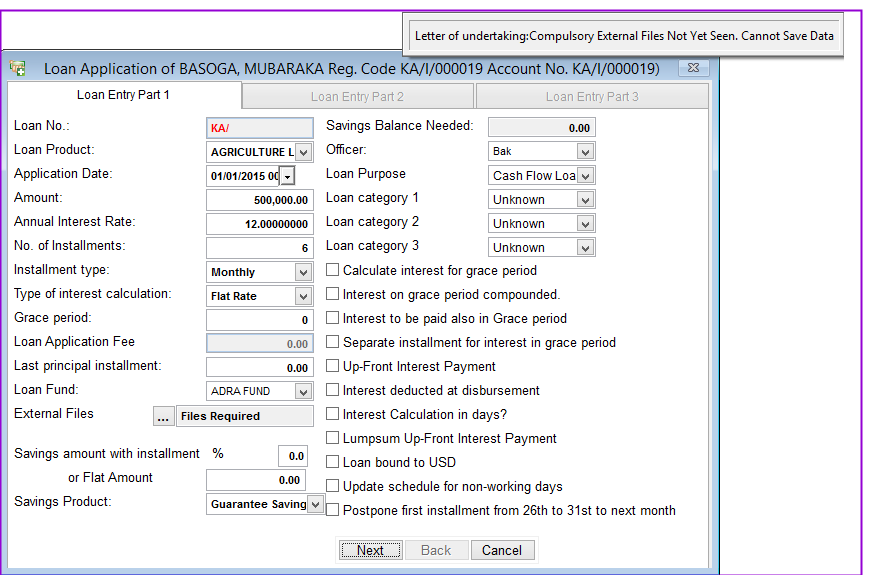

External Files: These are documents that may be required to facilitate the loan application process. For them to appear in the drop down menu, they need to have been entered under System/ Configuration/Loan products settings/Contracts for the selected loan product. For those documents which are compulsory, the option Compulsory must be ticked otherwise the following message appears at loan application.

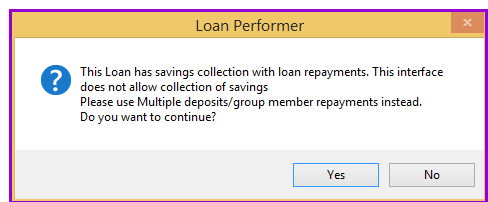

Savings amount with installment:Enter here the savings amount that is required along side the loan installments at the time of repayment.This can be a percentage of the principal amount of the installment or a flat amount. Once this option is used then the loan payment will only be through the multipurpose screen under cash/multipurpose deposits and not the main loan repayment screen. Otherwise the following message will be displayed

Savings product: Select the savings product from the drop down menu linked to the savings amount required with each repayment.

Note: When processing a group loan the above fields will not be available in this case LPF will give you those option on the third tab (Loan Entry Part 3 Groups).

Savings/Share Balance Needed:For loans that are linked to savings/shares, the amount of savings/shares needed in order to apply for the loan will automatically appear here according to the specifications set at System Configuration/Loan Product Settings/Guarantee Settings.

Note that if the loan product is linked to savings/shares under , and a Guarantee Settings specified percentage of savings/shares is required in order to apply for a loan. Loan Performer checks for the availability of funds on the client's savings/shares account.

Officer: This should be the name of the credit officer responsible for this loan application. Credit officers should be entered at the menu System/Configuration/Users. Select the appropriate name from the drop-down menu.

Loan Purpose: Select the purpose for which you are issuing the loan. The loan purposes should have been defined under Support Files/Loan Purpose

Loan categories 1, 2 and 3: Select the category of the loan from the corresponding drop-down menu. The loan categories should have been defined under Support files/Loan Categories.

Calculate Interest for Grace Period: If this option is marked, then the amount of interest for the grace period is calculated and added to the first loan principle due after the grace period. If this option is marked while the option "Interest to be paid also in Grace Period" is not, then the amount of interest for the grace period is automatically calculated and divided equally among all installments due.

Note that If "Calculate Interest in the Grace Period" and "Interest to be paid also in Grace Period" are both marked, the option to "Separate installment for interest in grace period" becomes active for the client to pay the interest in grace period as a separate installment from the principal as seen in the schedule below.

Interest on grace period compounded: When this option is ticked, the other options become inactive. All the interest to paid in the grace period will be added to the capital to calculate a new installment amount.

Interest calculation in days: When you select this option, the system will calculate interest in days even for flat rate loans. However for flat rate loans you should have also selected the option Recalculate Accrued Interest for Flat Rate Loans under System/Accounting/Calculate Accrued interest.

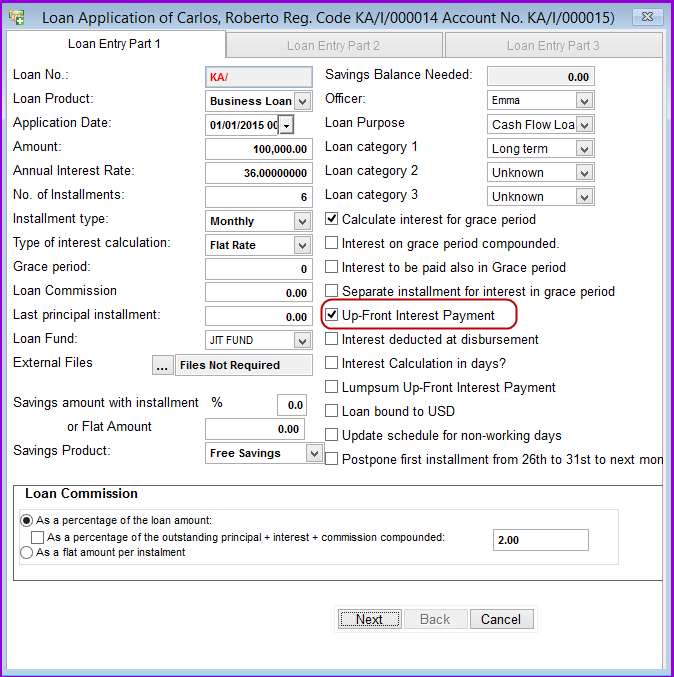

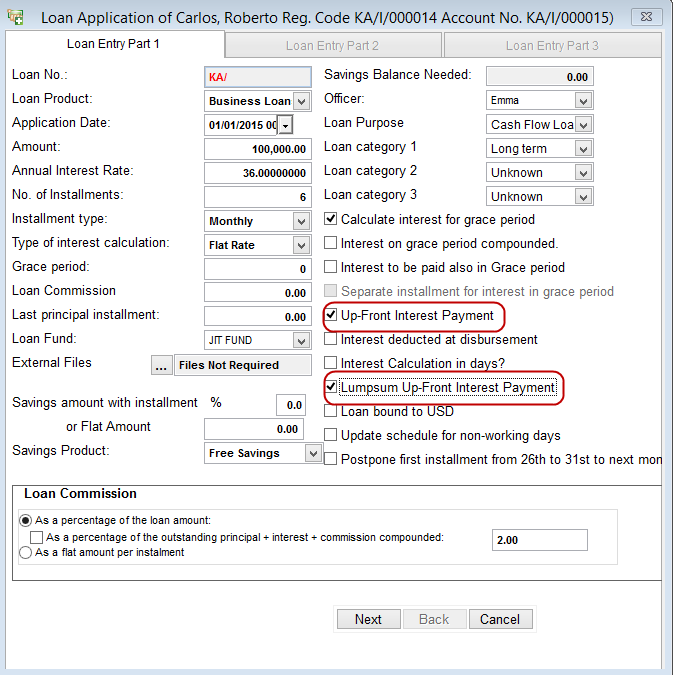

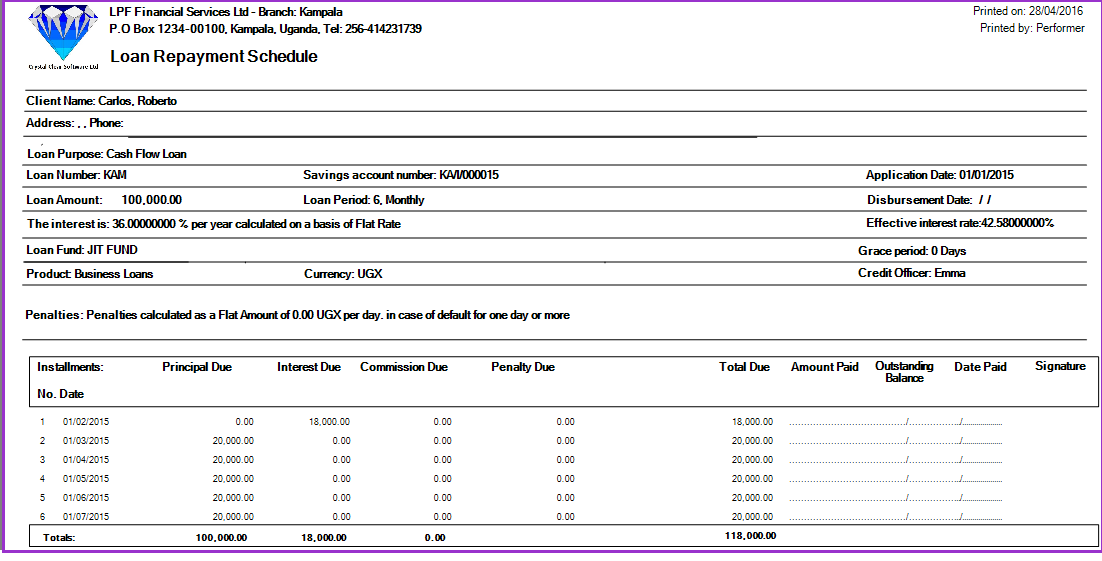

Up-front Interest Payment: As an example for this option, consider a loan of 100,000 UGX at an annual interest rate of 36% per year for 6 months but with an upfront interest payment and on flat rate basis (See the following image):

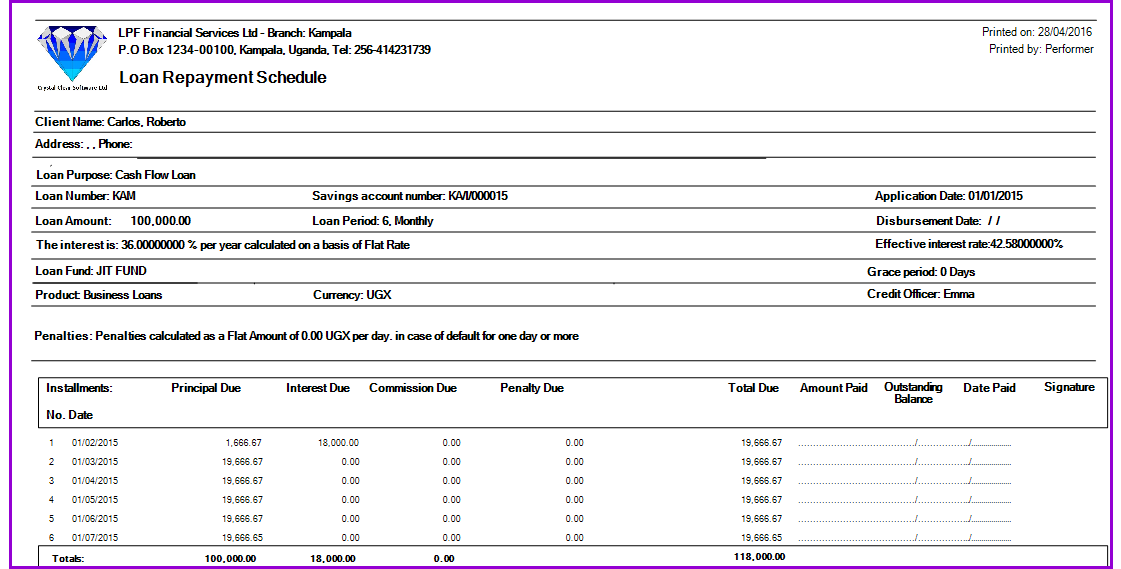

The repayment schedule appears as follows:

The repayment schedule generated shows that the first payment will only cover a small portion of principal payment and the entire interest payment while subsequent repayments will cover just the principal payments. Here the total paid at the end of each installment is equal for all installment dates as shown above.

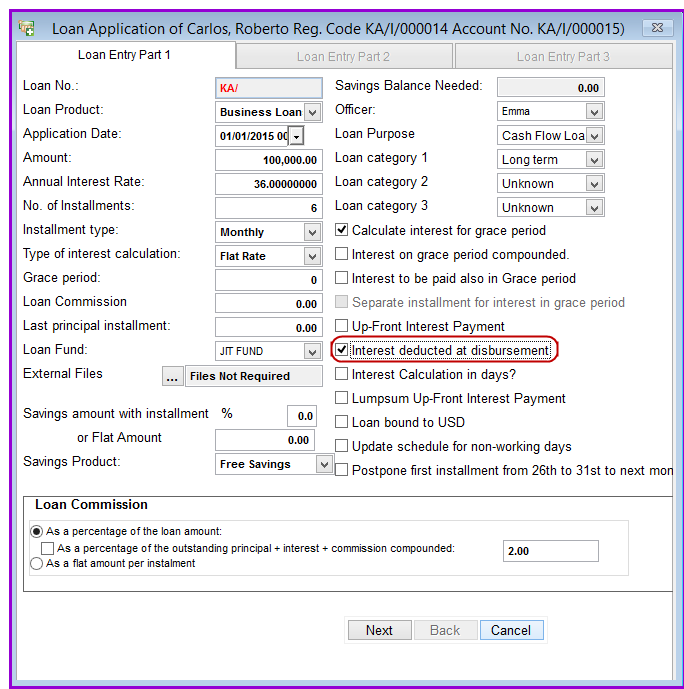

Interest deducted at disbursement: If this option is activated, the entire interest at the end of the loan term is realized at disbursement (See the following image):

The repayment schedule appears as follows:

As shown above, only principal is paid during subsequent 6 installments and in this case, the disbursement date is also the due date for interest payment.

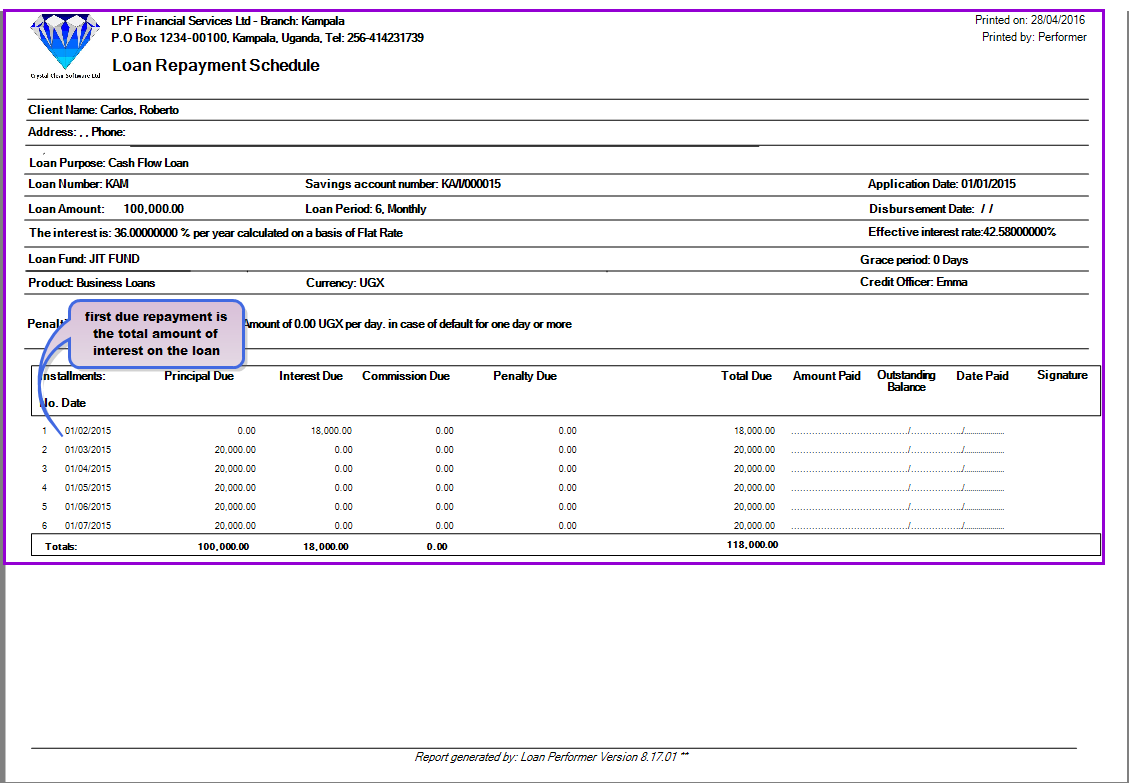

Lump Sum Up-Front Interest Payment: This option can only be used with the "Up-Front Interest Payment" option. Infact, when it is ticked the other option is automatically activated (See the following image):.

The repayment schedule appears as follows:

As shown above, first due repayment is the total amount of interest on the loan (it does not include the capital amount):

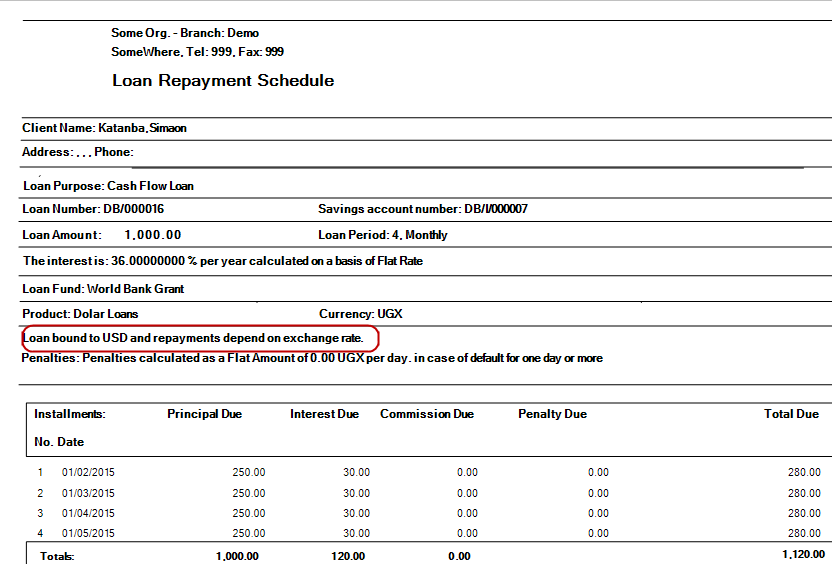

Loan bound to USD: When this option is ticked, the repayments of the loan will be subject to the exchange rate of the second currencyto which it is bound at disbursement.

For instance, if the exchange rate of the dollar to the shilling at disbursement of the loan is 1:1000, and at repayment it is 1:2000, a loan repayment of sh. 1050 will be: Rate at repayment / Rate at Disbursement * Repayment amount i.e. 2000 / 1000 * 1050 = 2100. The currency difference shall then be posted on the GL for currency differences at System/Configuration/Loan Product Settings/GL Accounts 1-2 Settings

Update schedule for non-working days: When this option is checked, the system will adjust the loan schedule to exclude non working days as set under System Configuration/Set Working Days

Postpone the first installment from 26th to 31st to the next month. Tick this check box for the first installment that falls between 26th - 31st of the month, to be postponed to the first working day of the next month.

Click on the Next command button to continue. You will be taken to the Loan Entry Part 2 tab.

Note:

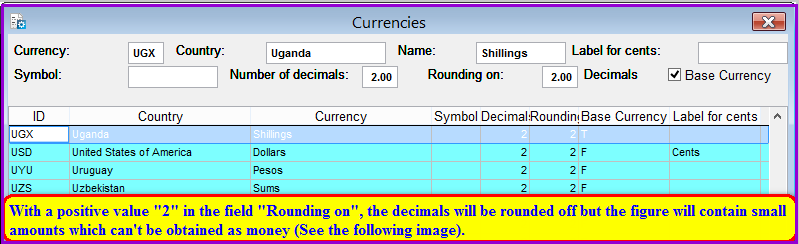

The field "Number of decimals" enables you to define the number of decimal places figures should have. Note that in LPF you can have a maximum of two decimal places. A positive value either "0", "1" or "2" entered in the field "Rounding on" does actually round off figures according to the number of decimal places specified. Therefore, enter in corresponding way either "0", "1" or "2" in those two fields in the menu Support Files/Currencies.

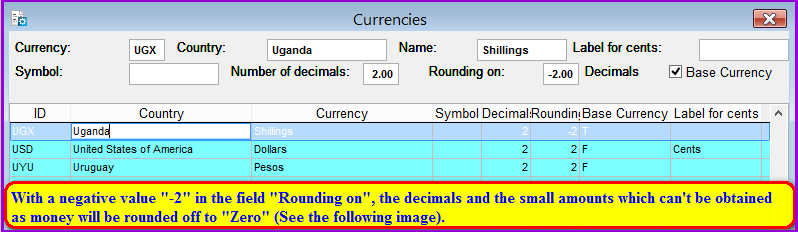

To get rid off decimals and small amounts you can not get as money, enter a negative value in the field "Rounding on". Then, amounts will be rounded off according to the number of decimal places specified regardless of the value entered in the field "Number of decimals".

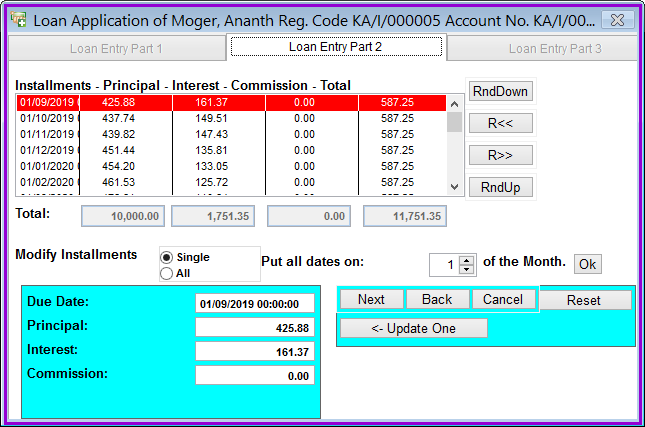

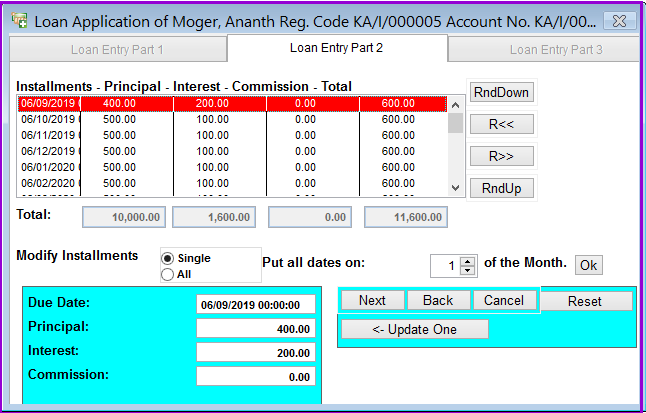

Therefore, the field "Rounding on" enables you to automatically get rid of small amounts you can't get as money e.g the amount "87" of the figure "587.25". For loans, when you enter a negative value e.g "-2" in the field "Rounding on", then according to the number of decimal places defined in the menu Support Files/Currencies, the system will round off the decimals and the small values of full amounts to zero. This is to say, "587.25" will be rounded off to "600" by deducting the necessary amount to round it off from the last installment of the loan in the menu Loan/Loan application/Loan Entry Part 2.

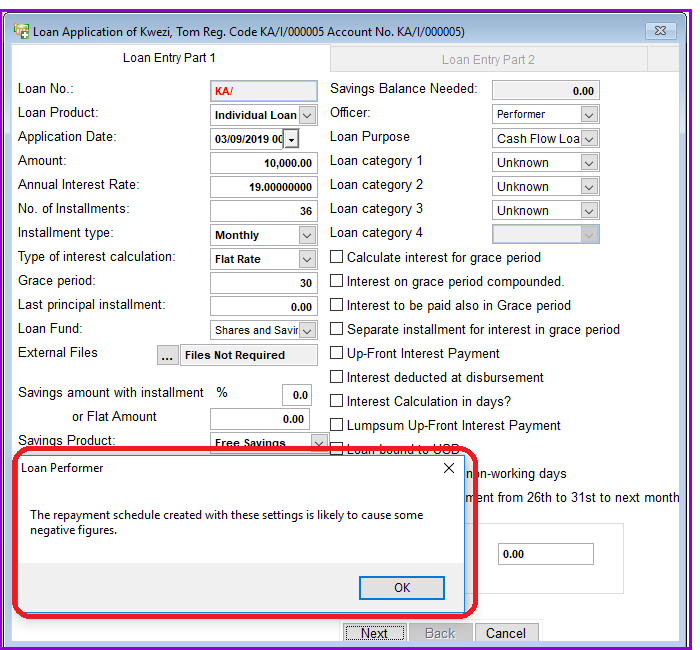

Since the values added when rounding off the amounts are deducted from the last installment of the loan, you risk ending up with negative figures for a repayment schedule with very many installments. In this case the repayment schedule will result into negative figures because of the number of installments, the system will return the following error message and the user will not be able to proceed with the loan application in the menu Loan/Loan application/Loan Entry Part 1.

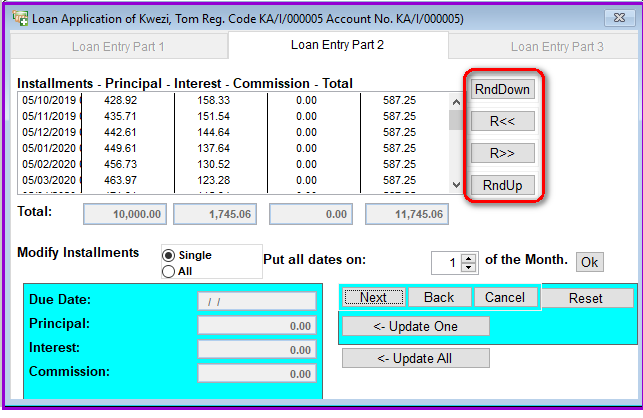

Note that Loan Performer also allows you to manually round off amounts by clicking the corresponding button in the menu Loan/Loan application/Loan Entry Part 2.

RndDown: Click on this button to manually round off the amounts of the repayment schedule to smaller amounts starting with the decimals. The small values deducted will be added to the corresponding amount of the last installment of the loan.

R<<: Click on this button to manually round off the amounts starting with the decimals. The small values added will be deducted from the corresponding amount of the last installment of the loan.

R>>: Click on this button several times to return to the original amounts of the repayment schedule. that some loan installments may have amounts that may not be practical to pay.

RndUp: Click on this button to manually round off the amounts of the repayment schedule to higher amounts starting with the decimals. The small values added will be deducted from the corresponding amount of the last installment of the loan.